Democracy’s Edge: Contested Reality

When old models fail, new models arise; the transition is rarely smooth.

This essay is Part II of a series examining Democracy’s structural failure modes and prospects. Each essay is designed to stand on its own. Other series essays are listed at the end.

Elite Overproduction and the Struggle for Collective Orientation

In the first essay in this series, we summarized Peter Turchin’s structural-demographic model, which examines how long-term patterns of population growth, economic surplus, and elite formation generate oscillating cycles of political stability and instability.1 These dynamics recur throughout recorded history and are not the product of any particular political structure.

While it is theoretically possible that future social structures might escape these cycles, none have yet done so convincingly. Attempts to abolish economic or secular cycles through utopian schemes have typically made matters worse.

Viewed through Turchin’s framework, most Western societies have entered a disintegrative phase: a period characterized by increased intra-elite competition, popular immiseration, reduced cooperation, fragmentation of authority, poor state finances, and a growing risk of political ruptures and conflict. These conditions may also apply in China; Turchin and his team plan to release a study on China's structural-demographic state before the end of 2026.

In the West, many citizens have a growing, intuitive awareness that something fundamental is breaking down. When turning to the press or political sense-makers for answers, this awareness is not typically met with clarity; instead, the infosphere is awash with many shallow, incoherent, and even actively deceptive explanations.

Developing a deeper understanding of these forces is not pessimism; it’s a refusal of default outcomes and superficial narratives. Discovering new ways to think about the world can help restore a sense of both individual and collective agency in an age when this has become disconcertingly elusive. This is a key point; we will return to it more explicitly in future essays.

Disintegrative phases are not historical anomalies; they are not the result of moral failure or poor leadership, although they can and do intensify both. This leads to a familiar error: blaming the various “bad people” who rise to prominence at such moments distracts individuals and societies from more durable problem-solving. Neither Trump, Starmer, Macron, nor any other unpopular world leader is an adequate causal explanation for what we are going through.

Once a society enters a disintegrative phase, it has no choice but to navigate the crisis. The key question now is how to navigate our current disintegrative stage wisely and emerge from it better off than when we entered it.

Periods of disintegration are inherently dangerous, but they are also the moments when systems that are no longer fit for purpose can be exposed and, potentially, replaced by more adaptive ones. That said, we should proceed with caution here: history has taught us that this process is never easy, linear, or guaranteed.

Dialectical materialism foreclosed adaptive societal learning by framing social progress as both predictable and historically inevitable. National Socialism’s concept of mythic racial destiny also tried to create a sense of predestined inevitability, producing equally catastrophic consequences. Both offered moral cover for repression and destruction in the name of progress.

The greatest risk in disintegrative periods lies not only in structural-demographic forces themselves but in how societies respond to them.

It’s important to note that these “secular cycles” last for many decades: the causes and effects build up slowly over time. Our current disintegrative phase did not start yesterday, and it will not be over tomorrow.

The Wealth Pump as an Engine of Instability

In Turchin’s model, economic surplus inevitably generates a structural wealth pump: a mechanism through which capital accumulation and elite overproduction interact to allocate an increasing share of economic surplus upward, faster than the overall economy grows. Thomas Piketty has summarized this simply as r > g (the return on capital exceeds the rate of growth).

As the number of elite aspirants rises, competition for positional goods intensifies, reinforcing the wealth pump and making capital concentration a structural outcome that persists regardless of intentions or ideology.

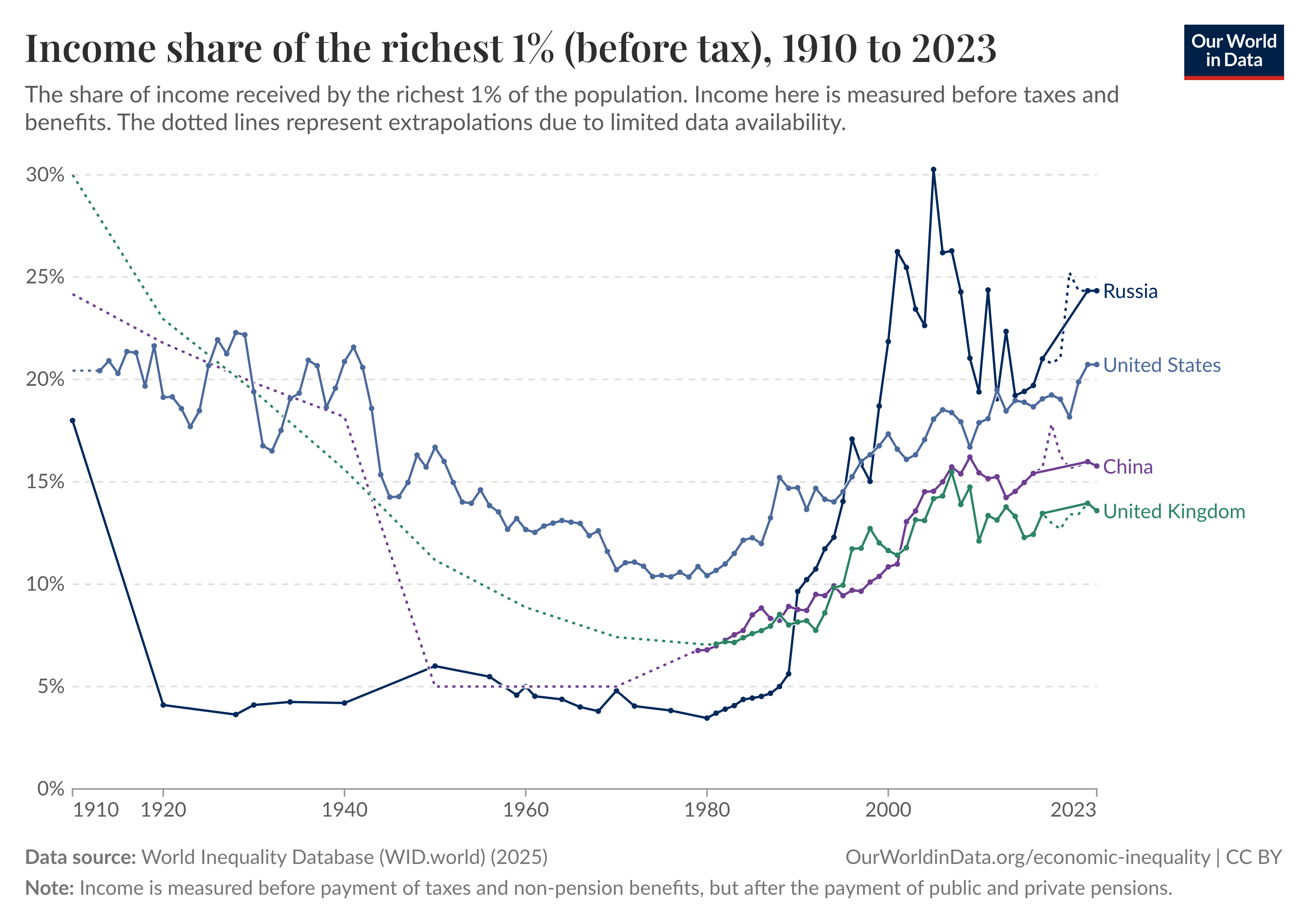

So long as a wealth pump is operating, it does not matter how much the overall economy grows or productivity expands. Surplus will tend to concentrate in the hands of those who control allocation, whether through markets, bureaucracies, or force. For this reason, wealth pumps recur across complex societies of many kinds, including both the United States and the Soviet Union.

While the data in the graph above appear to show lower inequality in the USSR, this largely reflects how inequality was structured and concealed: not through private wealth accumulation, but through differential access to housing, goods, political protection, and informal privileges that did not register cleanly in official income statistics.

Many proposals claim that abolishing private capital accumulation solves the wealth pump. Historical experience suggests more caution: in non-democratic societies, the allocation of power and status tends to reappear in bureaucratic forms that are less legible to outsiders.

While many optimists have pointed to an AI-driven productivity surge as a solution to this problem, Turchin’s wealth pump model suggests otherwise. It is highly likely that AI-driven productivity gains will lead to greater capital concentration, both because of the AI industry’s structure and because any economic growth that does not directly address the mechanics of the wealth pump will, by definition, continue to operate within a broader “wealth pump political economy.”

As Turchin has noted, the wealth pump generally coincides with popular immiseration.

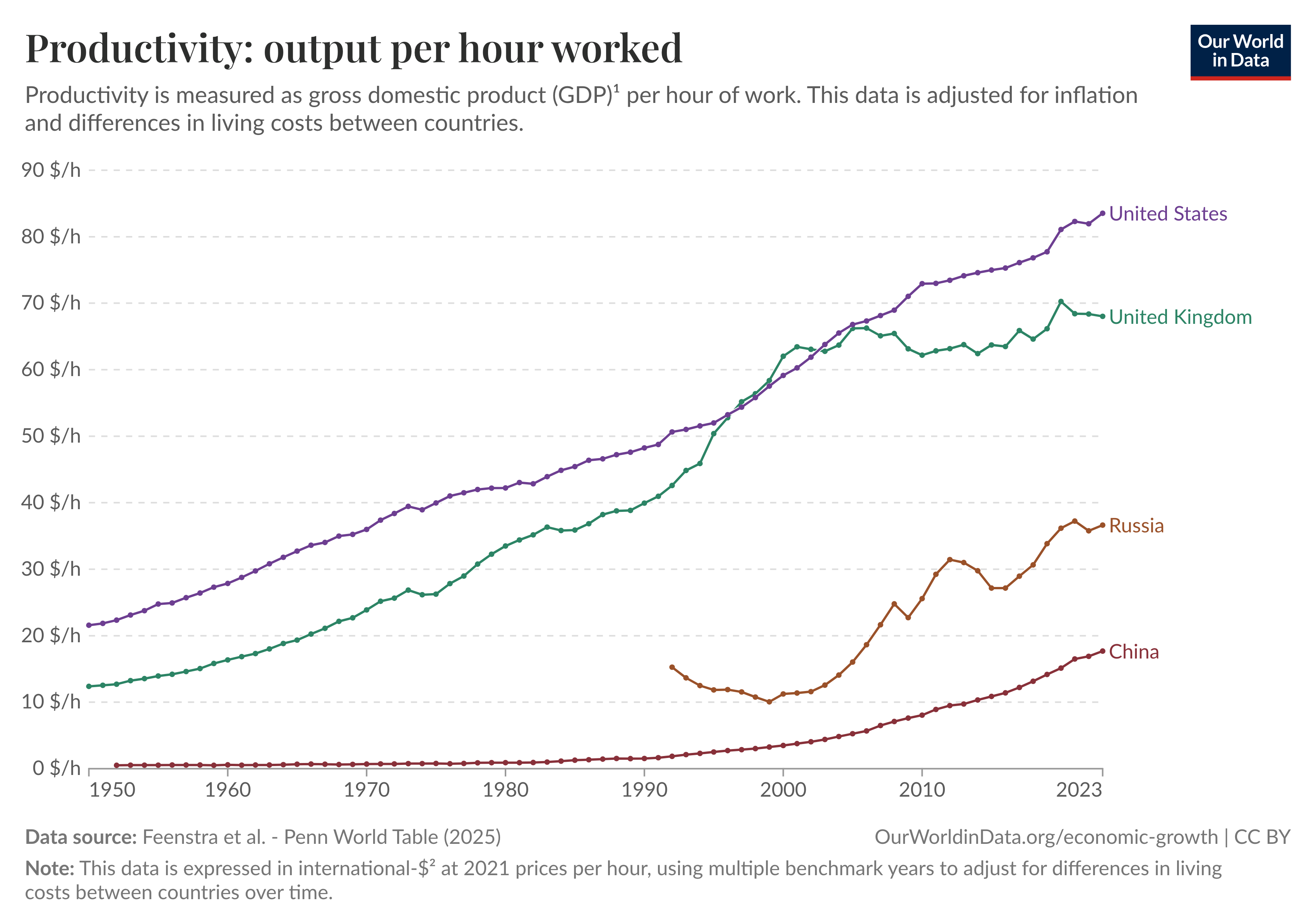

This is not a rejection of AI-driven productivity growth; such growth may be necessary to escape the current age of discord. But an AI boom is not a silver bullet that can resolve the disintegrative phase on its own. Absent wise and intentional policy design, increased productivity is more likely to accelerate inequality and instability than to produce shared prosperity. Since 1970, growing productivity in major economies has not reversed capital accumulation at the top. Workers have become more productive, but the benefits accrue mostly to capital.

2008: The Canary in the Coal Mine

The 2008 financial crisis was a moment in recent history that most people were happy to move on from.

From the typical citizen’s perspective, an incomprehensible financial hurricane hit; economists and bankers had emergency meetings with the politicians, and a series of confusing rescue deals was put together. Many people suspected that these deals were deeply unfair to ordinary people. However, as full employment returned, house prices and retirement accounts recovered; most people simply let it go. Older people did not lose their nest eggs. In subsequent years, however, buying a house became increasingly out of reach for younger people.

The proximate cause of the 2008 crisis was a collapse in the MBS (mortgage-backed securities) market. For those unfamiliar with the details, there is no better summary than the movie “The Big Short.”

In this essay, we will go beyond proximate explanations to view 2008 through a broader structural-demographic lens. In doing so, we can learn something important about our financial system, both then and now.

The Wealth Pump in Action

Starting in the 1970s, capital managers (banks, hedge funds, etc.) sought ways to generate higher returns amid a maturing economy. As intra-elite competition intensified, so did the search for financial returns that could no longer be satisfied by the “real economy” of productivity growth. Perhaps unsurprisingly, financial tools were therefore created to provide outside returns to financial insiders that far exceeded the underlying rates of economic growth.

In the run-up to the 2008 financial crisis, banks increasingly used financial structures that dramatically expanded credit without a corresponding increase in real economic output. Mortgage-backed securities and collateralized debt obligations had transformed household mortgages into tradable assets that could be repeatedly leveraged inside the financial system; in the early 2000s, they went into overdrive.

While real activity occurred—homes were built—the buyers’ ability to service those home loans depended increasingly on continued asset appreciation rather than wage growth. Rising home prices enabled refinancing, further borrowing, and additional financial intermediation, inflating the nominal value of the housing stock far beyond what the underlying economy could support in the long run.

In isolation, bundling mortgages into securities was not inherently problematic. Monetizing the income stream from a pool of loans is a routine financial practice. The problem arose when these securities were systematically mispriced for risk and then used as collateral to justify lending far in excess of the underlying mortgages’ values.

By treating bundled household debt as low-risk assets, banks were able to borrow against it, increase leverage, and expand the financial sector’s total money supply. In a fiat currency system, new money enters the economy through specific channels; when those channels run through asset markets and financial intermediaries, it tends to amplify wealth concentration by benefiting the first recipients and existing asset holders.

When we talk about “financialization of the economy”, this is what we mean. As demand for these MBS and CDOs grew, lending standards significantly deteriorated to generate more mortgages to package, further amplifying the cycle.

The result was a classic bubble: an expanding asset base untethered from the economy’s capacity to generate value. As long as asset prices continued to rise, newly created money flowed upward—to financial institutions, executives, and asset holders—allowing elite competition and institutional routines to persist without confronting the system’s growing top-heaviness. The system appeared coordinated not because participants shared a coherent understanding of risk, but because rising asset prices and concentrated financial rewards suppressed incentives to question the underlying models.

“Those of us who have looked to the self-interest of lending institutions to protect shareholders’ equity — myself included — are in a state of shocked disbelief.”

“I found a flaw in the model that I perceived as the critical functioning structure that defines how the world works.”

— Alan Greenspan, testimony before the U.S. House Committee on Oversight and Government Reform, October 23, 2008.

Before the crisis hit, most of the public went along with the status quo because a majority were homeowners, and on paper, their assets were appreciating. Those outside homeownership were often drawn in through increasingly appealing (but imprudent) lending practices—zero-down loans, teaser rates, and cash-at-closing incentives—leaving little immediate incentive to oppose the system while it appeared to be working.

The government was deliberately underwriting a lot of this activity because the politicians wanted to create more homeowners: a laudable goal so long as the home owners could actually afford the payments on those homes.

While this wave of financial engineering would ordinarily have produced visible consumer inflation, it largely did not. That period coincided with China’s increasingly rapid integration into the global manufacturing system, which supplied the West with an unprecedented volume of low-cost consumer goods. Large-scale offshoring of industrial production—plastics, metals, glass, electronics, textiles—placed sustained downward pressure on consumer prices, even as financial leverage and asset valuations expanded rapidly.

China’s reliance on abundant, low-cost coal with high energy return on investment further reduced production costs, allowing Western policymakers to frame offshoring as both economically efficient and environmentally beneficial under territorial emissions accounting, despite the shift of energy-intensive production to coal-powered supply chains abroad.

At the same time, a meaningful share of the surplus generated by China’s export-led growth was recycled into U.S. financial assets. Facing capital controls and periodic domestic uncertainty, Chinese households and firms sought to diversify into dollar-denominated stores of value, including overseas securities and U.S. real estate. Some of these movements are difficult to observe cleanly in headline public statistics, either because they appear in residual balance-of-payments categories or because holdings are routed through offshore custodians and financial centers.

This recycling of global surplus capital reinforced U.S. asset inflation—particularly in housing—further decoupling asset prices from domestic wage growth. The result was a self-reinforcing loop: suppressed consumer inflation alongside accelerating asset inflation, sustained by the system’s continued ability to absorb and concentrate financial gains without immediate disruption.

“I’m not running a business for profit. I’m running it for the good of the syndicate.”

— Milo Minderbinder, Catch-22 (Joseph Heller)

Why the Wealth Pump Eventually Produces Financial Crises

The concentration of wealth in fewer and fewer hands raises expectations of further wealth concentration among the holders of capital. To the individual holder of capital, this seems entirely rational. During “integrative cycles,” without a large surplus of aggregate elite expectations, the desire for outsized returns helps grow the overall economy by creating incentives for the formation of productive businesses; during periods of disintegration, the same beliefs and behaviors become destabilizing for society.

One way societies postpone the consequences of wealth concentration is through debt. Public debt expands to sustain services and social stability as more households fall behind; private debt expands to preserve consumption, asset prices, and the appearance of growth when wages and productivity can no longer support the same trajectory.

Debt can delay rupture, but it does not dissolve the underlying imbalance. It preserves surface stability by borrowing against the future; often while further inflating the asset values that benefit those already positioned at the top.

Eventually, debt service becomes a constraint. At that point, the system faces a forced repricing—either through inflation, default, austerity, or crisis—because the wealth pump has outgrown the society’s capacity to carry it.

As Turchin notes in Ages of Discord, the last comparable wealth-concentration crisis peaked in the 1920s–30s. In the United States, a grand bargain between private capital and the state helped the country traverse disintegration without systemic breakdown; others, notably Germany, failed to achieve such a bargain, opening space for extremism.2 In the US, a key element was the partial dilution of concentrated ownership, something that appears politically unlikely today.

Wealth Concentration at the Top is not a Conspiracy; it’s a Sign of Intensified Competition

As the number of elite aspirants outpaces available positions during a disintegrative stage, competition intensifies and increasingly aggressive behavior becomes rational in the pursuit of power, wealth, and positional goods. The internal struggles between the German aristocracy and the Nazi Party from 1933 to 1945 illustrate this dynamic: established elites were unwilling to pursue “German greatness” with the same extremity as aspiring Nazi elites, for whom radical escalation was a pathway to rapid advancement from the lower middle classes.3 As Richard Evans notes, the rhetoric of “German greatness” often masked naked competition for power, with Nazi officials constantly vying with one another for influence while looting whatever they could seize both within the Reich, and in the occupied territories.

One symptom of this tension was the number of plots and assassination attempts against Hitler, many of which were backed by elements of the old aristocracy. Nominally, Nazis and aristocrats co-mingled within the military high command, but beneath the surface there was deep and persistent distrust. The war forced a degree of collaboration between these two groups that would not otherwise have occurred, a dynamic we will return to at the end of this essay.

Returning to our current moment, well-established firms continue to grow through long-standing business practices and accumulated capital, while newly minted elite aspirants lack legacy power and therefore seek rapid career acceleration through sectors that reward speed, leverage, and abstraction. As intra-elite competition intensifies, concern for broader social or economic impact erodes. Under these conditions, industries where value is highly abstracted and competition is extreme—particularly finance and technology—become fertile ground for ethically questionable business models and even outright fraud.

For example, digital advertising fraud expert Dr. Augustine Fou has shown, across repeated empirical audits, that a majority—and in some cases a large majority—of digital advertising spend is lost to non-viewable impressions, automated traffic, and outright fraud. When waste and fraud are combined, Fou estimates that over half of global digital advertising expenditure fails to reach real human audiences.

This is not a new pathology. The 2008 financial crisis was not the only time financial crimes were committed; it was simply the case that irresponsible risk-taking and fraud grew so large that they came close to bringing down the entire economy. The end of that crisis did not resolve the underlying structural-demographic pressures that contributed to it. Absent a decisive move to relieve the pressures we have discussed, 2008 will not be the last crisis of the current era.

During our current age, finance creates short-term stability while generating long-term problems. Financial institutions that appear to be driving economic growth are also serving as accelerated wealth-pump mechanisms for both elite aspirants and legacy elites.

They are concentrating wealth faster than they are creating it.

For several decades prior to 2008, debt expansion and financialization functioned as compensatory mechanisms: they prolonged the wealth pump, absorbed elite competition by creating large amounts of new paper wealth, and delayed the political consequences of an emerging structural imbalance.

This arrangement did not resolve elite overproduction; it concealed its effects. It allowed interpretive fragmentation to grow while preserving the appearance of coordination and growth.

What a Rupture in the Wealth Pump Looks Like

The wealth pump cannot expand indefinitely because it depends on the continued reproduction of the productive and institutional systems it extracts from. Beyond a certain point, capital accumulation undermines those systems—reducing investment in productive capacity, institutional trust, and social stability—thereby eroding the very surplus the pump requires to operate.

The 2008 financial crisis did not mark the end of the wealth pump, but it did mark the moment when the system’s internal stress could no longer be plausibly denied. The resolution of that crisis was explicitly designed to keep the pump running, making it likely that another rupture will follow at some point.

What failed in 2008 was not merely a debt cycle, but the representational system that had allowed financialization to outrun the real economy. When leverage could no longer be rolled forward, the epistemic fragmentation produced by elite overproduction was forced into the open; no longer abstract or discursive, but operational. What had previously been absorbed as volatility was revealed as a model failure.

One of the most perceptive treatments of this moment appears in the film Margin Call.

The point of breakdown is captured succinctly by the bank’s CEO, John Tuld:

Tuld: What I’m guessing your report here says… is that considering the, shall we say, bumpy road we’ve been on the last week or so, that the figures your brilliant co-workers up the line ahead of you have come up with don’t make much sense anymore, considering what’s taking place today.

Interpretation: Tuld immediately recognizes that the models that the bank has been using to make money for years are now broken. In fact, as we learn later in the movie, he had been expecting this event for a long time and was already prepared to act once he saw the signal clearly enough. He understood the economic cannibalism the bank was engaged in, and during a speech at the end of the movie, he explains that it’s an indelible force of history, beyond anyone’s direct control. This is why he’s able to enjoy his newspaper and a glass of wine as the crisis unfolds around him: he knows it is all beyond his control, and he will sleep soundly knowing that at least he and his bank will survive the storm.

Tuld arrives on the scene, in the middle of the night, at the decisive moment of potential institutional failure. His team has just realized that their risk maps no longer help them navigate the territory. Everyone has essentially frozen: nobody knows what to do, not because they lack information, but because they don’t know how to orient to that information to turn it into effective action.

Tuld’s intervention is as rapid as it is decisive: he’s the only one in the room who’s not frozen, and he clearly needs to unfreeze everyone else quickly if the bank is to survive. He does this by arguing vehemently with the head of trading, Sam (played by Kevin Spacey). This move is not accidental: everybody in the room respects Sam, and if Tuld can get Sam on board with the new plan, then he can pivot the entire organization to a new strategy in just a few hours. This is exactly what he does.

Tuld’s task is not moral or ideological; it is representational. His job is to impose a new interpretive frame quickly, under duress, and restore the capacity for coordinated action, however costly the consequences. At one point, he clarifies his role in what is to come:

Tuld: I’m here for one reason and one reason alone. I’m here to guess what the music might do a week, a month, a year from now. That’s it. Nothing more. And standing here tonight, I’m afraid that I don’t hear a thing. Just…silence.

Tuld: So, now that we know the music has stopped, what can we do about it?

The “music” Tuld hears is not the market, but the models that underpin the participants’ ability to trade inside that market. When those models can no longer interpret a workable reality for the trading desks, markets seize up, and asset prices go into freefall. Survival then depends not on moral virtue or predictive certainty, but on the willingness to act decisively once inherited representations have failed.

In real life, this insight was institutionalized rather than improvised by those far-sighted enough to plan for it. At Bridgewater, Ray Dalio designed systems around the recognition that patterns recur across history, even when timing cannot be predicted. Both Dalio and Peter Turchin converge on the same conclusion as the fictional John Tuld: complex systems fail in recognizable ways, but never on schedule.

In Margin Call, Tuld’s brutal reassertion of representational authority occurs just in time to save the institution. In history, that timing is often missed. As I argued in Strategic Blindness, French political and military leadership in 1940 possessed ample information but failed to replace a collapsing framework quickly enough to act. By the time the rupture was acknowledged, there was no time to implement more adaptive ones: the window for response had closed.

This is the hinge between institutional survival and collapse: not knowledge, but orientation. In times of crisis there must be rapid re-orientation under extreme duress.

How Entire Societies Lose Their Grip on Reality

Every stable social order relies on model compression: shared ways of simplifying an overwhelmingly complex world into forms that allow coordination and action at scale.

Physics compresses reality into equations that remain valid within defined domains, even though the underlying granular dynamics remain computationally irreducible. Biology compresses reality into signals and heuristics that organisms can reliably act on without incurring the arbitrary energetic cost of modeling the world in full. Engineering compresses complexity into models that are sufficiently accurate for action within known tolerances: explicit error bounds that define how much deviation a system can safely absorb.

Tolerance is not imprecision. It is a deliberate choice of model fidelity, sacrificing granularity to enable repeatable action, on the assumption that the operating environment remains within known limits.

Social systems do the same. Laws, institutions, professions, and norms compress complexity into thresholds that trigger action. Intelligence agencies decide what counts as background chatter versus a credible warning. Militaries distinguish exercises from preparations. Governments judge whether instability is manageable volatility or systemic failure.

These thresholds govern escalation. They determine when institutions act, who is authorized to act, and what costs are considered acceptable. As long as these compressions preserve what actually matters, disagreement remains bounded and coordinated action is possible.

Breakdown begins when reality changes faster than institutional frameworks can update. Under elite saturation, updating the model becomes politically costly: local actors bear the risk of being wrong, while incumbents benefit from preserving failing representations that protect budgets, status, and asset values.

As a result, institutions may possess more information than ever—more data, more reports, more dashboards—yet lose the ability to agree on what that information means. Signals blur. Warnings are reclassified as noise. What once demanded action becomes ambiguous or politically inconvenient.

This is not hypothetical. It is what happened in France in 1940, when commanders observed German armor massing but interpreted it through a World War I framework that assumed time, deliberation, and linear escalation. The failure was not informational, but interpretive.

When institutional models no longer map to reality yet remain in place because they protect elite positions and nominal value, coordination gives way to fragmentation. Competing interpretations proliferate, responsibility diffuses, and decision-making slows or freezes—not by choice, but because the inherited frameworks are no longer capable of producing clarity.

This is exactly what happened in the financial crisis of 2008.

This is the most dangerous phase of institutional failure. Societies lose shared orientation even as factions within them regain internal coherence and act with increasing confidence. Authority persists, but legitimacy thins. Action becomes either indefinitely delayed or abruptly coercive, driven by simplified narratives rather than updated understanding.

Yet this crisis is unavoidable. No society adapts by preserving representations that no longer work. The breakdown of shared models is the precondition for new ones to emerge. The question is not whether reality will be contested, but how that contestation is governed.

History shows the pattern clearly. The Copernican revolution shattered an Aristotelian cosmos that had linked observation, theology, and authority for centuries. The printing press destroyed the Church’s monopoly on interpretation and multiplied epistemic elites faster than institutions could absorb them. The Reformation transformed interpretive conflict into political fragmentation and war. In each case, recompression eventually occurred—not through deliberation, but through coercion.

The danger has never been the breakdown itself.

It has been how breakdown is managed.

What this moment requires is not certainty, but restraint in the exercise of power.

How structural pressures lead to coercive impulses

A common failure during disintegrative phases is falling back on familiar ideological themes from either the left or right, which promise clarity through simplicity and order through coercion or exclusion. Instead of addressing the root structural issues, these ideologies act as mechanisms of forced compression, quickly restoring order by limiting acceptable interpretations and eliminating dissent through in-group purity tests and other forms of enforced solidarity.

This pattern is well documented. Hannah Arendt observed that totalizing ideologies emerge not primarily as belief systems, but as instruments for restoring order under conditions of institutional and interpretive collapse. By reducing complex social reality to a single internally coherent explanatory frame, ideology enables mass coordination to resume even as it severs the feedback loops that connect belief to external reality—producing what she described as a deadening banality rather than genuine understanding.4

Structural-demographic research reaches the same conclusion from a different angle. As intra-elite competition intensifies, factions narrow the range of acceptable explanations to consolidate support. Charles Tilly, studying revolutions and state formation, shows that when states lose the capacity to adjudicate competing claims through institutions, they substitute coercion and exclusion for integration.5

Political Islam fits this pattern more closely than is often acknowledged. Olivier Roy argues that modern Islamist movements arise less from theological revival than from the collapse of secular interpretive authority and the failure of post-colonial states to integrate expanding educated elites.6 Under these conditions, Islamism operates as a recompressive ideology: it restores legibility by subordinating political disagreement to moral certainty and redefining citizenship in terms of doctrinal conformity.

As with communism and fascism, the appeal is not complexity, but closure; not adaptation, but legibility for populations and for states.

The High Price of Repressive Unity

Extreme political simplifications come with a steep price: they collapse the institutional complexity required for modern cultural and economic life. A modern economy cannot provide broad prosperity under political systems that replace distributed decision-making, legal predictability, and adaptive feedback with ideological fiat: whether it’s Marxism-Leninism, fascism, kleptocracy, or Islamism.

For example, Nazi Germany, despite its obsession with technology and its theatrical fixation on the future, failed to build a self-sustaining economy. The vibes were modern, even futuristic, but the governing mechanisms were medieval: growth depended on coercion, confiscation, forced labor, and the systematic plunder of conquered territories. Genghis Khan would have recognized their system, if not their weapons or uniforms.

War was not a deviation from Nazi economic logic but a critical element required to fuel it. The Nazi war on Europe was, at its core, the greatest act of murderous armed robbery the world has ever seen.

Despite enormous growth in recent years, China has not fully escaped the flattening effects of Communism. Its growth after 1970 happened exactly where Communist policies were loosened: through market pricing, local experimentation, and integration into global capital flows. Many ongoing structural issues—capital misallocation, information suppression, and political interference—are closely linked to the elements of ideological control that the CCP still maintains.

There is no easy escape for global society at this point. We need to recognize which parts of disintegration are unavoidable, which are healthy, and how societies can navigate epistemic rupture without increasing human suffering. The focus isn’t on maintaining an old system, but on transitioning to a more adaptable one that can thrive amid the challenges and conditions ahead.

Premature Closure

When inherited models are failing, societies experience intense pressure to decide anyway. Ambiguity becomes intolerable. Competing interpretations feel destabilizing. Leaders are asked to “take a position,” institutions are urged to “send a signal,” and narratives harden long before models have been sufficiently reality-tested.

This is what premature closure looks like.

We need only look at the rush to judgment over the shooting of Renée Good in Minneapolis. In the US, this case became a national narrative battle from the moment it was first reported. Both sides raced to eliminate nuance in the struggle for narrative dominance; under intra-elite competition, dominance translates into mobilization, fundraising, and institutional leverage. The reality was messy and multi-causal, but the journalists and politicians are rewarded by presenting simplified stories rather than balanced judgments.

Premature closure occurs when a society resolves interpretive uncertainty by forcing a single explanation into authority before there is sufficient evidence, adaptation, or feedback to justify it. Instead of allowing models to compete, revise, or fail on their own terms, power is used to select one account of reality and suppress the rest.

It is tempting precisely because it works, at first.

Premature closure restores coherence quickly. Disagreement is forced underground. Roles become legible again. Chains of command reassert themselves. Action resumes. The system feels stable because uncertainty has been eliminated, not because the problems that led to the breakdown of the old models have been understood.

History is full of such moments. Weimar Germany offers a stark example. Faced with economic collapse, elite fragmentation, ideological saturation, and a population exhausted by ambiguity, the Nazi regime imposed a brutally simplified explanatory model: national humiliation had a single cause, social decay had a clearly defined set of enemies, and renewal required unity enforced through obedience. Political paralysis ended almost immediately. Authority centralized. Mass mobilization became possible.

But this kind of coherence is maladaptive in the longer run.

By converting contested interpretations into enforced orthodoxy, premature closure shuts down error correction at the moment it is most needed. New information is no longer integrated; it is treated as subversion. Deviations are punished rather than examined. Learning does not merely slow; it stops. The system can no longer adapt; it can only persist or break.

In Germany’s case, as internal contradictions accumulated and reality resisted the imposed model, adaptation became impossible. Escalation was the only remaining option. War was not an accident of ideology, nor a deviation from policy, but the mechanism through which unresolved internal failure was displaced outward.

This is why premature closure so often leads to catastrophe. It trades short-term order for long-term fragility. It replaces exploration with obedience. And once adopted, it tends to escalate: the more reality resists the imposed model, the more coercion is required to maintain it.

This is the bridge to authoritarianism, conflict, and war.

War as Recompression

When inherited models fail and premature closure sets in, societies face a narrowing set of options. Ambiguity becomes intolerable. Internal disagreement feels destabilizing. Yet stagnation is equally unacceptable. Action must resume, even if understanding has not.

Under these conditions, war emerges not as a failure of reason, but as a response to a specific structural problem: the loss of shared orientation.

War performs recompression.

One clarification is necessary. The breakdown of shared orientation does not mean that societies remain permanently disoriented. In practice, recompression continues, but it fragments. Rival factions impose internally coherent interpretations of reality that restore coordination, legitimacy, and purpose within their own ranks, while remaining incompatible with those of other groups. Each faction regains agency locally, but shared orientation at the societal level is not restored; it is partitioned. This condition is unstable. Civil conflict is not inevitable, but it becomes structurally possible because action is once again feasible while mutual intelligibility has collapsed. War resolves this instability by imposing a singular interpretive frame across the entire system.

War collapses interpretive plurality into a single authoritative frame. It answers contested questions of legitimacy, competence, and loyalty with outcomes rather than arguments. Victory validates the model. Defeat discredits it. Ambiguity disappears because survival itself becomes the metric of correctness.

This is why war (both within and between states) has so often resolved elite overproduction across history. It reduces elite numbers through death, demotion, disgrace, and exhaustion. It reallocates authority quickly, concentrating power in institutions capable of command. It restores coordination by making obedience rational again, not because consensus has been achieved, but because dissent has become too costly.

War also simplifies causality. Complex, multi-factor failures are reinterpreted as external threats. Internal contradictions are displaced outward. Social strain is converted into mobilization. Economic dislocation becomes sacrifice. Political paralysis gives way to emergency authority. A society that could not agree on what was happening suddenly agrees on what must be done.

This is why war so often feels clarifying at the outset. It resolves the intolerable pressure of epistemic overload by enforcing closure at scale. Competing models do not need to be adjudicated; they are selected by events. War does not require shared understanding in advance. It manufactures it afterward.

But this efficiency comes at an extraordinary cost.

War restores orientation by annihilating exploratory capacity and forcibly overriding rival recompressions with a single, system-wide frame. It does not solve the underlying problems that produced disorientation; it suppresses them. The learning that occurs is brutal and narrow: what survives is taken as correct. What fails is erased. Future adaptation becomes harder, not easier, because error correction has been conflated with defeat.

This is why war is both effective and tragic as a recompression mechanism. It works quickly. It scales reliably. And it leaves societies less capable of navigating the next epistemic rupture without repeating the cycle.

The deeper risk facing advanced societies today is not that war might break out by accident, but that it may once again become the fastest way to restore societal structure under pressure to fragment.

Avoiding war, then, is not primarily a matter of restraint or goodwill. It is a design problem.

Unless societies can find non-violent ways to re-establish shared orientation under conditions of elite saturation and epistemic fragmentation, war will continue to perform that function by default.

The goal is not consensus at all costs, but the preservation of conditions under which collective learning remains possible while inherited frameworks are breaking down. The failure mode to avoid is treating social breakdown itself (whether through ideological purification, repression, or war) as a legitimate substitute for adaptation.

Governing Breakdown Without Forcing Closure

If the argument of this essay is correct, then the central danger facing advanced democracies today is not disagreement, polarization, or even institutional dysfunction in isolation. It is the temptation to resolve epistemic overload through premature closure: to restore coherence by force when shared orientation has broken down.

Disintegrative phases cannot be skipped. Elite overproduction cannot be wished away. Competing interpretations cannot be eliminated without cost. The only real choice societies have is how they navigate these periods of contestation, and whether recompression occurs through learning or coercion.

The difference matters enormously.

Societies that preserve the capacity for collective learning under pressure do not eliminate conflict. They manage it. They resist the urge to convert uncertainty into orthodoxy. They maintain institutional spaces where rival models can be tested against reality rather than against purity tests. They delay irreversible commitments long enough for feedback to arrive. And they tolerate a degree of ambiguity that feels uncomfortable precisely because it keeps adaptation possible.

This is not indecision. It is a restraint on the exercise of power.

The alternative is faster and more legible. Forced closure restores order quickly. It clarifies enemies, simplifies causality, and makes obedience rational again. It also forecloses learning at the moment it is most needed. When reality continues to resist the imposed model, escalation becomes the only remaining tool. This is how societies slide from paralysis into authoritarianism, and from authoritarianism into conflict and war.

Avoiding that trajectory does not require consensus, virtue, or perfect foresight. It requires institutional designs and political norms that treat contestation as a signal to slow down rather than to clamp down; that distinguish between loss of control and loss of orientation; and that resist treating social breakdown itself as evidence that more force is the answer.

The task, then, is not to restore a lost unity or to defend inherited models past their usefulness. It is to govern breakdown without mistaking it for collapse.

Democracy’s edge is not defined by how much disagreement it can suppress, but by how much uncertainty it can withstand without resorting to coercive recompression. Whether modern democracies can meet that test remains an open question.

We should all resist the temptation to view this as a purely “left - right” issue: we see exactly the same dangers emerging in Trump’s America and in Starmer’s Britain, at opposite ends of the political spectrum.

What is clear is that if we fail, war may once again do the work we refused to design for.

Conclusion

Everything described above happens before runaway escalatory spirals; and therefore before most societies recognize how much danger they are really in.

The real risk is not that elites compete, that interpretations diverge, or that institutions hesitate. The risk is that when recompression finally becomes unavoidable, the only tools left are coercion and war.

Part III of this series will begin with a blunt premise: if war remains the most reliable recompression mechanism available to complex societies, what other tools can perform this task while avoiding both internal and external war?

The task ahead is to imagine and test forms of governance that can absorb epistemic rupture without enforcing closure; tolerate ambiguity without paralysis; and recompress shared reality without annihilating the very capacity to learn.

Whether modern democracies can do this is not yet known. What is known is that history offers little mercy to societies that postpone the question until violence answers it for them.

We are very lucky to have such engaged and thoughtful readers. If you have any observations to share or questions to ask, we strongly encourage your participation in the discussion of these important topics.

Related Essays

References

Peter Turchin and Sergey A. Nefedov, Secular Cycles (Princeton, NJ: Princeton University Press, 2009).

Peter Turchin, Ages of Discord: A Structural-Demographic Analysis of American History (Princeton, NJ: Princeton University Press, 2016), 211–255.

Richard J. Evans, The Coming of the Third Reich (New York: Penguin Press, 2004), 249–303; Richard J. Evans, The Third Reich in Power, 1933–1939 (New York: Penguin Press, 2005), 33–92.

Hannah Arendt, The Origins of Totalitarianism (New York: Harcourt, Brace & Company, 1951), 468–479; Hannah Arendt, Eichmann in Jerusalem: A Report on the Banality of Evil (New York: Viking Press, 1963), 287–294.

Charles Tilly, European Revolutions, 1492–1992 (Oxford: Blackwell, 1993), pp. 7–12, 27–33.

Olivier Roy, The Failure of Political Islam (Cambridge, MA: Harvard University Press, 1994), pp. 1–9, 23–31, 61–72

I think your analysis is very clear and correct, but the elite over production angle just confuses me. Yes, I see the concentration of wealth. Yes, I see the increasing conflict over access to this concentration of wealth. Yes, I see the increasing creation of losers that turn against the current political order due to this. But that does not look like an elite overproduction mechanism. That looks like centralization followed by sclerosis trapping those orders into paths they can't navigate out of. The "elite overproduction" looks less like any kind of causal mechanism, then it does a description of one aspect of this malfunctioning process. I don't see any reason why these people (the aspirants) can't be kept out indefinitely and history has many examples of this. Caste systems and rigid orders tend to be the norm. So the idea of it being some kind of cyclical inevitability is hard for me to swallow.

Its the attempt to navigate out of this state of affairs that leads to revolutions, not forces and elite overproduction, but the revolutions that developed are not inevitable. The Meji did it, Prussia did it, and other have, too. The Anglo/western political tradition just refuses to countenance this, which is really odd when you think about it.

Hi Simon

Great essay, hard to disagree

I’m actually on comments for a personal reason. I’m Nic Stratton’s, finally found, father. Your god son’s grandfather. Lovely to meet you. Really enjoying my new family. . You and I have many similarities. Try TED talk:https://www.youtube.com/watch?v=A5wIBRuFAS8